China’s Stimulus Sparks Massive Opportunity Amid Historic Short Squeeze: A Hedge Fund Perspective

China’s long-awaited stimulus finally arrived—and with it, chaos erupted. What began as a seemingly standard policy announcement quickly spiraled into one of the biggest market squeezes in recent memory. Trading volumes exploded, brokerages reported glitches, and some of the most sophisticated quant funds in China found themselves caught in a brutal short squeeze, forced to liquidate at the worst possible moment.

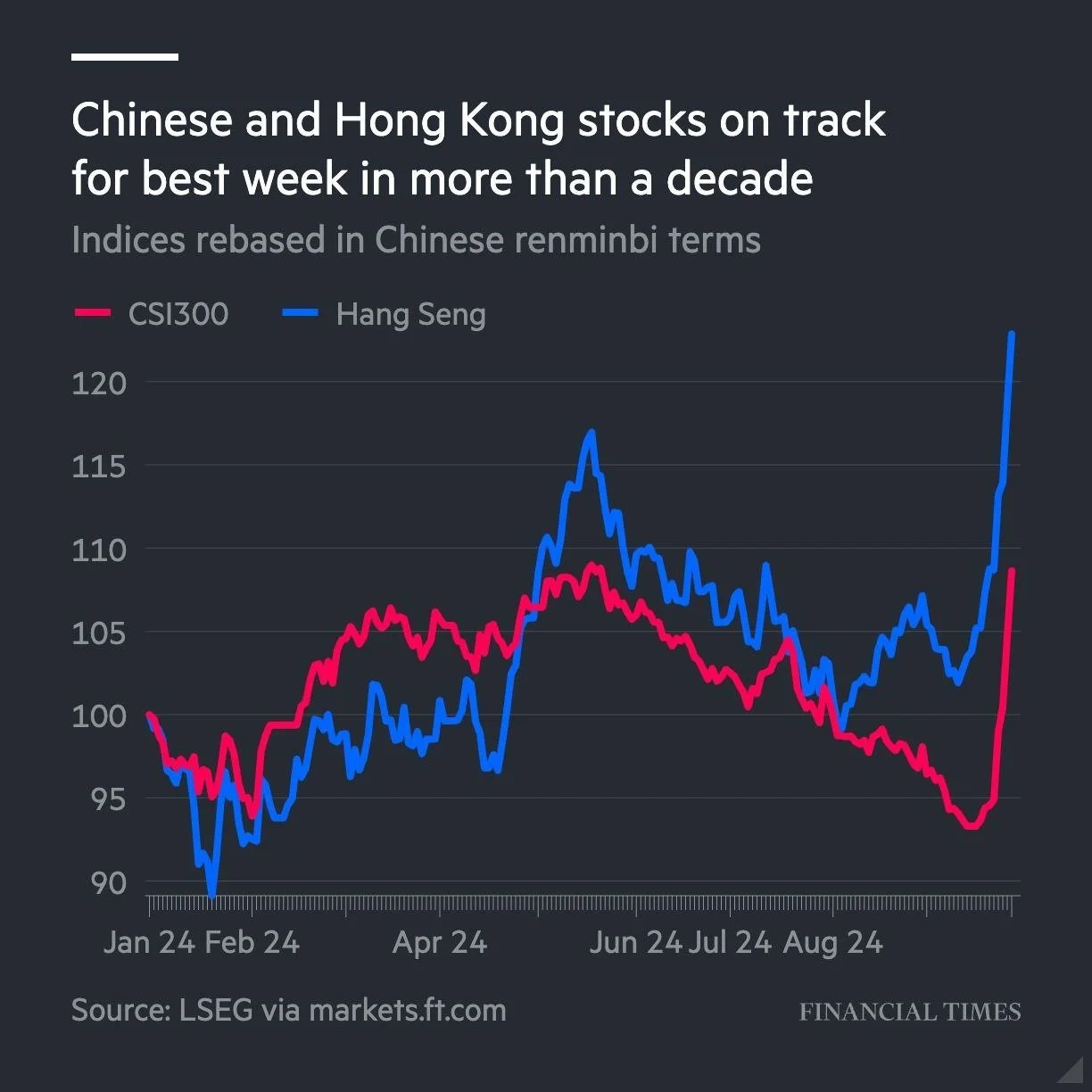

The result? The largest weekly rally in Chinese equities since 2008 and a sudden reversal of sentiment that no one saw coming. With hedge funds caught wrong-footed and investor positioning at record lows, the stage is set for a major revaluation. But is this just a short-term reprieve, or could it be the start of something much bigger?

For those watching closely, it might just be time to bet on the latter.

The Macro Backdrop: From Stimulus Hopes to Reality

For months, markets have been waiting for Beijing to roll out a meaningful stimulus package to revive its faltering economy. But each time, hopes fizzled out as the government opted for small, incremental measures that failed to inspire confidence. This changed last week, when the People’s Bank of China (PBoC), alongside the National Financial Regulatory Administration (NFRA) and the China Securities Regulatory Commission (CSRC), surprised markets with a coordinated wave of monetary easing.

The PBoC cut the 7-day reverse repo rate by 20 basis points and lowered the Reserve Requirement Ratio (RRR) by 50 basis points, injecting hundreds of billions of yuan into the banking system. They also introduced reductions in mortgage rates, relaxed property regulations, and hinted at further fiscal support to follow. The move was a clear signal that Beijing is finally shifting from cautious policy tweaks to more assertive action. The question on everyone’s mind: is this just a temporary boost, or is China setting the stage for a longer-term recovery?

A Turning Point, but Not a Bazooka

While these measures have reignited interest in Chinese assets, they were not a “bazooka” of fiscal firepower. Instead, Beijing’s approach appears more calculated, seeking to stabilize the economy without overcommitting resources. The government is likely holding back its full arsenal for later, especially given the looming uncertainty of the U.S. election and its potential impact on global trade dynamics.

Despite the restrained rollout, the market’s reaction was explosive. Trading volume across Chinese equity markets roared to levels 4x above the 20-day average, and a glitch in the Shanghai Stock Exchange temporarily stalled trading, further amplifying the scramble. This surge in activity wasn’t driven by retail traders or momentum chasers—it was the result of forced liquidations among highly leveraged quantitative funds, many of which had been running market-neutral strategies shorting Chinese indices.

The Short Squeeze That “No One” Expected

Most global funds had remained deeply underweight Chinese stocks, citing persistent growth concerns, the property sector slump, and geopolitical risks. With Chinese equities making up just 4.5% of the gross exposures in some hedge fund books—down to 5-year lows—the setup was ripe for a violent squeeze. The sudden policy shift flipped sentiment on its head, turning a routine announcement into a market-moving event as heavily shorted futures contracts were forced to unwind.

The massive rally in Chinese stocks was compounded by a broader repositioning among local investors, further driving prices higher. This wave of forced buying has raised hopes that Beijing may finally be serious about propping up the economy, but skepticism remains. After all, Chinese authorities have hinted at stimulus measures before, only to pull back when conditions appeared to stabilize.

The Road Ahead: Fiscal Measures or False Dawn?

If Beijing follows up with aggressive fiscal stimulus—potentially involving large-scale investments in infrastructure, social spending, and consumption subsidies—the rally could gain even more momentum. An unusual September Politburo meeting further fueled these expectations, as policymakers emphasized the need for more coordinated action. However, if the next wave of stimulus underwhelms, the market could reverse just as violently.

This delicate balance between hopes for a structural recovery and fears of policy disappointment makes the current environment both a minefield and an opportunity. For hedge funds, understanding this dynamic is key to positioning correctly and avoiding getting caught on the wrong side of another squeeze.

With the macro backdrop rapidly shifting, it’s time to dig into which sectors and stocks could benefit the most from China’s renewed push for stability.

Unpacking the Recent Market Action: Short Squeeze, Glitches, and Forced Liquidations

What started as a routine day in the Chinese equity markets quickly turned into a chaotic roller coaster that no one was prepared for. Hedge funds and quant strategies that had been comfortably positioned for downside risk found themselves on the wrong side of an unexpected surge. By the time the dust settled, a chain reaction of forced liquidations and market-wide short covering had propelled Chinese stocks into one of their biggest weekly gains in over a decade.

The Catalyst: Policy Surprise Meets Record Low Positioning

The initial trigger was a surprise announcement by the People’s Bank of China (PBoC) and other regulators, signaling stronger-than-expected support for the financial system and property market. The measures—though not a game-changer in terms of absolute scale—exceeded market expectations, prompting a frenzy of buying across all major indices. For a market starved of positive news, this was the jolt that kicked off the rally.

But what turned a routine rebound into a violent squeeze was the structural setup beneath the surface. Hedge funds, quants, and systematic traders had built up substantial short positions in index futures and maintained low exposure to Chinese equities. The pessimism was justified: Chinese equities had been battered by sluggish growth, ongoing real estate sector distress, and a lack of decisive government intervention.

According to Goldman Sachs research, exposure to Chinese equities in many hedge fund books had fallen to just 4.5% of total gross exposures, and net short positions were building rapidly. With sentiment skewed so heavily to the downside, even a modest policy shift was enough to flip the script.

The Shanghai Stock Exchange Glitch: The Spark That Lit the Fuse

As the policy announcements began to sink in, buying pressure quickly overwhelmed the order books. Within the first hour of trading, turnover hit an astonishing 710 billion yuan ($101 billion), and the Shanghai Stock Exchange started experiencing glitches in processing orders. This wasn’t just a technical hiccup—it was the catalyst that trapped bearish quant funds at the worst possible moment.

High-frequency and quantitative strategies, which rely on Direct Market Access (DMA) for quick execution, found themselves unable to cover their shorts or unwind positions as the market surged. With some DMA strategies running at up to 10x leverage, the sudden breakdown in trading systems left them exposed to margin calls and forced liquidations.

As the index futures moved from a persistent discount to a premium, quants running market-neutral strategies were forced to close their index shorts, further amplifying the upward spiral. By the time the system stabilized, many of these funds had incurred severe losses—reminiscent of the 2015 stock market chaos in China, when similar glitches led to massive liquidations and panic buying.

The Magnitude of the Squeeze: A Flashback to 2008

Friday’s rally wasn’t just any squeeze—it was the biggest weekly surge in Chinese equities since 2008. This explosive move is even more surprising when viewed against the backdrop of extreme bearish positioning. With most global funds underweight and many quants outright short, the scramble to cover created a classic short squeeze that fed on itself, pushing prices higher and higher.

Hedge fund exposures to China had reached 5-year lows, as uncertainty around growth, property market distress, and geopolitical tensions kept most players on the sidelines. The sudden influx of $580 million in inflows into China ETFs (the second-largest in a decade) served as both a signal of panic and a warning that the market consensus had become too crowded on the short side.

Direct Market Access (DMA) Strategies: The Achilles Heel

For many Chinese quant funds, the Achilles’ heel was their reliance on DMA strategies, which typically involve holding long positions in individual stocks while shorting index futures. When the index futures surged above fair value, these funds were hit from both sides—unable to sell their long positions fast enough and trapped in rapidly deteriorating short positions.

According to sources within the industry, some funds faced margin calls that forced them to liquidate their long holdings at a loss, exacerbating the problem. The combination of high leverage, illiquid markets, and technical glitches created a perfect storm that caught even the most sophisticated players off-guard.

Implications for Hedge Funds: Is the Pain Over?

While the immediate pain for bearish quants may be over, the broader implications are just starting to unfold. Forced liquidations and short squeezes tend to have a lasting impact on positioning and sentiment, often leading to prolonged reversals as traders adjust their books. With so many funds having been flushed out, there is now a vacuum of short positions that could create a positive feedback loop if buying momentum continues.

This also means that the opportunity is ripe for hedge funds willing to take the opposite view—accumulating long positions in beaten-down Chinese equities or building tactical long/short setups to exploit any volatility. As sentiment begins to shift and more funds are forced to reverse their underweight positions, the risk-reward skew for Chinese equities could be more favorable than it has been in years.

Key Takeaways: What Comes Next?

The recent short squeeze was driven by a perfect storm of unexpected policy measures, technical glitches, and extreme positioning. With many quants forced to liquidate, the path is now clear for further upside.

Long-term positioning remains at 5-year lows, suggesting there is significant room for reallocation into Chinese equities if sentiment stabilizes.

However, the volatility is unlikely to subside immediately. Any disappointment in follow-up fiscal measures could lead to another round of whipsaw action.

For hedge funds, the play now is to position tactically—taking advantage of the unwinding of short positions while staying nimble in case the rally runs out of steam. With policymakers hinting at more stimulus, and quant funds licking their wounds, the next few weeks could set the stage for a prolonged re-rating of Chinese assets.

A Calm After the Storm, or Just the Eye?

China’s sudden rally wasn’t just a flash in the pan—it was a stark reminder of how fast sentiment can shift when the tide turns. A cascade of forced liquidations, a scramble to cover shorts, and a market caught completely off-guard—what began as a surprise stimulus package turned into one of the most dramatic short squeezes in recent history.

But this isn’t just about quants licking their wounds. Beijing’s recent moves are more than a desperate attempt to prop up growth; they’re a signal of intent. With markets still reeling from the shock and positioning at historic lows, the question is whether this is the calm after the storm—or just the eye.

For investors who can navigate the chaos, this might be the start of a much bigger opportunity. The game now? Lean into quality names poised to thrive in a stabilizing China, while taking tactical shorts in distressed sectors that still have more pain to come. Because if Beijing’s next move is the long-awaited fiscal follow-through, this rally may just be getting started.

The stakes are high, but for those who get it right, the reward could be even higher. After all, in a market like this, fortune favors the bold.

The Content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained on our Site constitutes a solicitation, recommendation, endorsement, or offer by EF or any third party service provider to buy or sell any securities or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction.