Bear Market Fatigue: Are Investors Too Tired to Panic?

The current market state is leaving investors feeling fatigued as they try to navigate the ups and downs of a bear market. With the recent history of market crashes and rallies, many investors are wondering if they have the energy to ride out this current downturn.

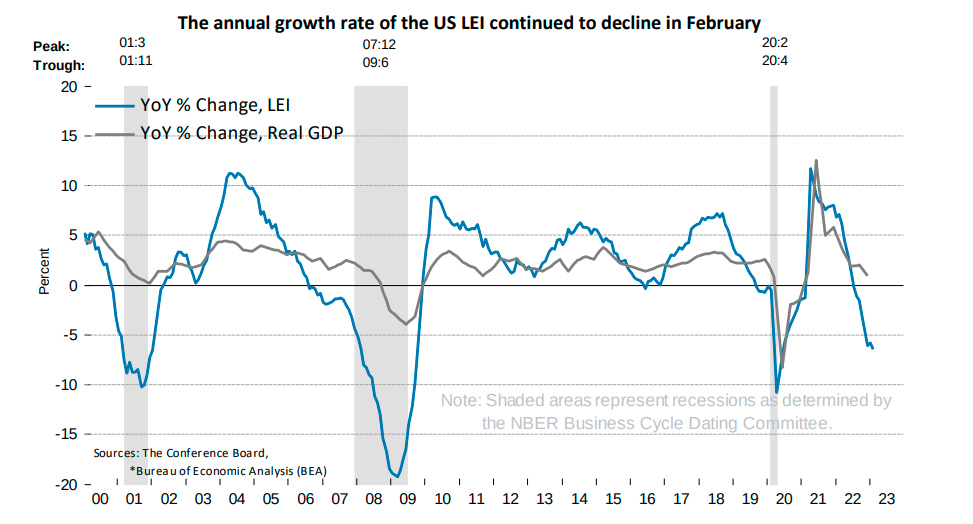

According to Justyna Zabinska-La Monica, Senior Manager of Business Cycle Indicators at The Conference Board, the Leading Economic Index (LEI) for the US declined for the eleventh consecutive month in February. This was due to eight out of the ten components showing negative or flat contributions, despite improving stock prices and a better-than-expected reading for residential building permits. Although the rate of decline has slowed down in recent months, the LEI still suggests a risk of recession in the US economy.

However, it's worth noting that the recent financial turmoil in the US banking sector is not reflected in the LEI data but could have a negative impact on the outlook if it persists. The Conference Board predicts that rising interest rates combined with declining consumer spending are likely to push the US economy into recession in the near future.

The S&P 500 has experienced 20 bear markets in the past 140 years, with an average peak-to-trough decline of 37.3% and an average duration of 289 days. According to history, the "average" bear market should have ended on October 19th, 2022, with the S&P 500 at 3005. However, this bear market has lasted longer than normal, but policy intervention has prevented a significant decline in price (the SPX low was 3577). Additionally, the biggest bull market recoveries, averaging 40% in 1 year and 54% in 2 years after lows, occur only after the largest declines.

One of the biggest concerns for investors is the possibility of a bear market rally. This is when the market experiences a temporary uptick, only to fall again shortly after. Many investors have been burned by these rallies in the past, as they thought they had hit the bottom of the market, only to see it fall further.

The recent collapse of commerical bank SVB has reignited discussions around the concept of "capitulation" and the possibility of a bear market bottom. Historically, market bottoms have often been marked by the last optimists giving up and selling shares at rock-bottom prices, creating a buying opportunity for new investors looking for bargains.

However, the idea that SVB's collapse will act as a catalyst for a rebound may be misplaced. While previous incidents, such as the collapse of Bear Stearns in 2008, have been followed by market rebounds, the historical parallels may not be strong enough to draw any conclusions. The situation with SVB is not as central to the market's current difficulties as previous collapses, and the current market state may be more complex than previous bear markets.

It is important to note that bear market rallies can be deceptive, as history has shown. The collapses of the Dow Jones Industrial Average after 1929 and the Nasdaq Composite after 2000 both saw significant declines of around 80% over three years, with several bear market rallies along the way that ultimately led to further losses for investors.

The collapse of the Dow Jones Industrial Average after 1929 and the Nasdaq Composite after 2000 both saw falls of about 80% over three years. Yet both also experienced several bear market rallies when the index recovered by 20% or more, only to continue falling.

In the case of Bear Stearns, the acquisition by JPMorgan arranged by the Fed in March 2008 did lead to a short-lived bounce in bank stocks, with a 15% increase over the next few days and an 11% increase in the S&P 500. However, the sell-off resumed, and bank stocks and the S&P 500 eventually bottomed out in March 2009 after a 51% drop from the bear market rally high.

Investors are becoming weary of the ongoing threat of a bear market, which often involves a series of rallies that can deceive them into believing that the market has hit rock bottom. The fear of missing out can lead to irrational decisions, such as chasing high-risk assets and following the crowd towards a potential crash. Even seasoned fund managers like Stanley Druckenmiller can succumb to this behavior. Typically, a bear market occurs in stages, with the first involving wealthy investors and the top 1% selling their positions, followed by overleveraged or mispositioned hedge funds in the second stage, and long-only funds unwinding and hedge funds adding shorts to hedge macro risks. This can prompt retail investors to follow suit and add short positions, ironically increasing the risk of a short squeeze as the left tail event takes time to materialize. In the third stage, a significant retail exodus is anticipated, but strong counter-trend rallies can entice investors back in, ultimately leading to a real crash when the risk emerges suddenly. Currently, we appear to be in the late stages of the second stage, and investors are experiencing fatigue and doubting their bearish thesis without a left tail event. Although the market has rebounded from its recent low during the regional banking crisis, the rally may continue if Q1 earnings exceed expectations, and if credit conditions do not deteriorate further, sales growth may hold up better than anticipated. Ironically, if this rally does occur, it may actually increase the probability for more downside surprises, as investors refocus on fundamentals instead of narratives.

“I was just an emotional basket case and couldn’t help myself”

“I can predict the movement of heavenly bodies, but not the madness of crowds.”

Sir Isaac was one of the initial investors in the South Sea Company (SSC), a firm with a monopoly to trade in the South Seas in exchange for assuming England's war debt. In 1720, he decided to sell his stake in SSC, making a handsome profit. However, he soon became a victim of greed when he saw the share price continue to rise and gave in to temptation, buying back in at three times the price of his original investment. Unfortunately, his decision proved to be disastrous, as he lost almost his entire life savings, which today would be equivalent to $6 million.

Higher For Longer?

After reaching a local low point in October 2022, the US equity market has remained relatively stagnant despite the collapse of SVB. Investors have shifted their focus from concerns about higher inflation to the possibility of a lower inflation environment, lower yields, and an economic slowdown. While investors are anticipating a potential Federal Reserve pivot that could result in rate cuts, the recent inflation data indicates that inflation remains significantly above the Fed's 2% target. As a result, the Fed is on track to raise interest rates by 25bps in May, which has been confirmed by this week's CPI number. If the CPI prints softer than expected, the need for a continued hiking cycle may be negated, which the Fed would welcome due to concerns around bank deposits and losses on HTM portfolios. However, core CPI inflation still runs at 5.1% on a three-month annualized basis, which is double the rate consistent with the Fed's 2% PCE inflation target.

Assuming that the banking sector remains stable, the Federal Reserve is likely to follow through on its projection of raising interest rates to 5.0-5.25%, as indicated in their dot plot. Despite the slow decline in inflation, particularly in the service sector, it appears that interest rates will need to remain elevated for a longer period of time, potentially resulting in the 2.5 rate cuts currently priced in to not materialize. The Fed is cautious about reducing rates prematurely, as it may risk reigniting inflation. The most recent FOMC minutes indicated that job gains have been strong, but inflation remains elevated. Despite the recent developments in regional banks, which may result in tighter credit conditions and potentially impact economic activity, hiring, and inflation, the Federal Reserve remains committed to its price stability mandate. The Fed aims to keep inflation low and stable over the long term, and it will continue to use its tools and implement policies to achieve this goal. Additionally, given that it takes time for the impact of rate hikes to affect real economic activities, the cumulative effect of monetary tightening may result in another wave of market volatility in both equity and bond markets as more economic data is released. Investors should be prepared for potential risk-off events to resurface, as the Fed remains cautious and vigilant about inflation risks and would only pivot if something broke, such as a credit event.

The market-based economy is efficient due to supply and demand determining capital allocation and consumption behaviors. Economic equilibrium is the state where market forces are balanced and prices stabilize. Prices indicate where the equilibrium is, and if prices are too high, demand decreases, while if prices are too low, demand increases. However, economic equilibrium is a theory because markets are dynamic, and the equilibrium is constantly evolving.

A Random Walk Down Economics 101

Economic 101 teaches us that economies function most effectively when they are in a state of equilibrium, and policymakers utilize their instruments to guide the economy towards that state. There are three necessary conditions for equilibrium: Spending and output aligned with capacity, debt growth aligned with income growth, and a normal level of risk premiums in assets relative to cash. However, none of these conditions currently exist. Nominal spending exceeds the output capacity of labor, leading to inflation. Reducing spending will lead to a downturn in real growth, creating a different imbalance. Interest rates are lower than nominal spending, leading to credit growth and spending, which contradict the tightening of monetary policy. Inverted yield curves offer no risk premium in bonds compared to cash, and equity pricing has very little risk premium in equities relative to bonds. The key variable in achieving equilibrium is the Federal Reserve's goal of 2% inflation, which requires reducing wage growth from 5% to around 2.5%. This can be achieved by reducing nominal spending and income growth to 3-5% and increasing the unemployment rate by at least 2%. Achieving these conditions requires a significant decline in nominal GDP growth and compressed profit margins, leading to double-digit earnings decline. Once these conditions are met, short-term interest rates should be stable for about 18 months until sustainable 2.5% wage growth, 2% inflation, and 2% real growth are attained. However, the current sequence of conditions suggests that the path to equilibrium has a ways to go, and the Fed's policy path is likely to be iterative and volatile, with tough choices and market volatility along the way. The initial move is to tighten to fight inflation during strong growth, followed by a pause that triggers a relief rally in assets, leading to a swift sentiment shift and investors chasing the herd towards a cliff. This cuts short the decline in inflation and requires a second round of tightening.

As mentioned earlier, curbing wage inflation is crucial to achieving the 2% inflation target, and this requires decreasing spending and raising unemployment to influence the labor market's supply/demand balance. Currently, businesses are facing negative profits and limited credit sources, resulting in reduced activity in several areas, including buybacks, mergers and acquisitions, capital expenditures, and hiring. To achieve sustainable 2% inflation, layoffs are necessary to cool the labor market and bring down wage growth. It's worth noting that in the past, an increase in the unemployment rate has often coincided with a decline in corporate earnings. To bring wages down, corporate earnings would need to decrease by about double digits. However, this hasn't happened yet, and most Wall Street analysts remain optimistic about corporate earnings, with a consensus estimate of a small 4% decrease in earnings per share during the weakest recession in 2023. This estimate is followed by a renewed surge to $242 by 1Q25, up 72% from the COVID low in 1Q21. Even though the proportion of above-consensus corporate guidance issuances for the US has decreased significantly over the past six months, the estimate for world EPS growth in 2023 remains positive at 8%, which is optimistic.

Earnings Recession?

In our previous note, we predicted that the Fed would have to tighten policy to combat inflation, which would result in a slowdown and hurt valuations. Now we are experiencing the second part of this prediction: the Fed is still hiking rates during the slowdown. The current consensus is that there will be a slowdown, but the magnitude of it may not be fully priced in. We are still in the early stages of an earnings recession, and while the consensus view earlier this year was that earnings would be significantly lower than expected, the economy is holding up better than anticipated and people are now less bearish about earnings. Looking at the S&P 500's forward 12-month earnings, it peaked at $240 in June 2022 and has since fallen to about $223, based on company guidance. Sell-side strategists are too optimistic at 210 to 215, and we could see a base case of 190 or as low as 170 in a recession. This significant delta will matter. Earnings revisions will likely continue to come down for the next few quarters, but this is now fully discounted. The market is trying to say that the worst is behind us, but earnings revisions won't necessarily improve from here. If the Fed remains in a "higher for longer" stance, the consensus forecast for earnings, even if valuations remain rich, will be affected. Investors are currently rewarding operational efficiency instead of sales growth, with a focus on things like lower inventory to sales growth, lower CapEx to depreciation, and lower labor costs as a percentage of cost of goods sold. This trend has been driving stock price performance, even though companies aren't growing to gain market share, but rather cutting costs to survive. However, this operational efficiency factor will only remain in favor until either prices come down or earnings improve. We believe companies haven't yet gotten ahead of the cost structure, which is out of whack with revenue growth. Eventually, valuations will need to come down to reflect the earnings risk. If valuations come down because they're too rich, we could see a double-digit downside for many stocks and even the major averages.

The root cause of the SVB crisis can be traced back to the post-financial crisis era when credit pipes were rebuilt in ways that made the financial system safer but also opened up new gaps. Banks, unable to find profitable uses for the deposits they received, started investing more in government bonds and government-guaranteed mortgage issuance, which accelerated during the pandemic due to a surge in deposits from monetary policies. Some banks took on more duration than others, and those that miscalculated how likely they were to hold on to their deposits and moved out on the duration curve are now struggling and failing.

Not a Credit Event, Yet

The collapse of SVB and some regional banks caused a series of risk-off events that prompted investors to reassess the risk of a recession, resulting in a decrease in bond yields and an increase in volatility. However, investors eventually shifted their allocation towards the technology sector, as lower bond yields tend to benefit high-growth and high-beta stocks. With the bank run easing, the Fed's temporary accommodative balance sheet is starting to tighten, and the future path is uncertain. Nonetheless, the markets have stabilized in recent weeks, thanks to two positive data points. First, the outflow of deposits from banks has slowed down, and small banks that lost over $100 billion in deposits following the SVB collapse saw inflows for the first time in late March. Second, inflows into money market funds have also slowed down, suggesting that the contagion from bank funding stress is being contained. Although regulatory risk remains a concern, this is mainly an earnings story, particularly for regional banks. The broader implications of this episode have decreased from a systemic issue to a pullback in credit availability, especially for low-quality smaller issuers. Private capital can partially fill this gap, and this is unlikely to escalate into a more significant economic concern.

However, the strain on the banking sector is happening without a credit loss cycle, which is unusual compared to past banking crises. The major banking crises in history, such as those in 1930, the S&L crisis in the 1980s, and the 2008-2010 crisis, were all driven by credit losses and had a significant impact on the availability of credit to the private sector. If the current stress on the banking sector combines with a credit loss cycle where loans start to default, it could have a double whammy effect that reinforces itself. This is similar to the savings and loan crisis, which was triggered by low short-term interest rates and low deposit rates, and borrowing at low rates and lending at higher rates. If there is a tightening due to inflation, as happened in the 1970s, and a similar yield curve, the credit cycle could come later and make things worse. The current situation could weaken banks and hurt them further if there is a growth move and credit losses associated with it, leading to a one-two punch similar to the savings and loans crisis.

Fade the Rally

According to a recent study by BofA's Michael Hartnett, he suggests fading SPX at 4200 and sees a potential bear market rally in distressed CMBS and regional banks due to extremely bearish sentiment. Hartnett believes that the stock market will attempt new lows in the next three to six months due to a confluence of factors, including history, policy, and recession. Currently, the Fed funds market pricing indicates an expected peak of 5% on May 3rd, followed by a 25bp cut on July 26th and 210bp rate cuts over the next 18 months. However, unlike previous years, inflation is now a reality, and global central banks are either "hawkishly holding" or hiking rates. The credit and stock markets may be too eager for rate cuts and not cautious enough about a potential recession. Historical data suggests that it is wise to "sell the last rate hike" in an inflationary environment as this was the correct stock market strategy during the inflationary periods of the 1970s and 1980s. During disinflationary periods, the average Dow Jones returns after the last Fed hike were positive; however, during inflationary periods, they were negative by 4.5% over the next three months and negative by 6.6% over the next six months.

Q1 earnings preview

While an average quarter is predicted, attention will be focused on guidance and tighter credit conditions affecting capital expenditures and share buybacks. Estimates are typically cut one quarter at a time, and the past two decades have seen quarterly EPS being reduced five to six times in a row before each season. The macro environment during Q1 was divided into two halves, with mixed macro indicators suggesting further weakness ahead.

Thus far, 22 early reporters, primarily in Consumer, Tech, and Industrials, have reported Q1 results, with a 70% correlation between early reporter beats and full-quarter beats. However, maintaining margins during a weakening demand environment is challenging despite companies announcing initiatives to cut costs.

Earnings are expected to surpass the economy in 2024 as earnings tend to recover stronger than they fall, resulting in a leaner cost structure and improved margin profiles. However, the consensus 2024 EPS of $247 (+12% YoY) seems ambitious. Tech earnings have been lagging behind S&P 500 earnings for the past 1.5 years, and a pull-forward in demand during COVID and potential cost reversal from globalization may challenge Tech earnings both cyclically and secularly.

Bridgewater CIO Karen Karniol-Tambour has pointed out a discrepancy in the pricing of equity and bond markets. Equity pricing assumes that profits and the economy will not experience a significant slowdown. However, profits have already started declining, and it may be challenging to sustain ongoing strong profits without any impact on the economy. If equity pricing is correct, it would be unlikely for rates pricing to be accurate. This is because, in a strong profit environment, the Federal Reserve would not quickly ease interest rates with high inflation. Conversely, rates pricing could be plausible if the economy collapses, and inflation continues to decrease. The summary of these markets appears implausible, as the behavior of actors in response to the other market's conditions does not align.

“I think the biggest mispricing in markets today is really the combination of markets. It’s not one market that’s mispriced. It’s that the different things that are priced into various markets can’t coexist at the same time.”

To summarize, the current market presents challenges for investors who may feel worn out by the prolonged bear market. The uncertainty and fear of extended downturns may cause some to question their bearish stance or become complacent during periods of low volatility. While bear market rallies can occur, causing perma-bears to turn bullish and leading to FOMO "melt-ups," these rallies are susceptible to sharp reversals or failures due to risk factors such as earnings recession, credit events, and the legging effects of rate hikes and quantitative tightening during an economic slowdown. As disciplined investors, it is crucial to stick to our investment process, which, in our case, involves reducing risk and adopting a defensive position* in the latter half of 2021. Our process still sees significant downside risk in the future. As bear market fatigue sets in, it may be an excellent opportunity to revisit the fisherman's principle: “expect nothing but follow the process that we have developed through trial and error.” We cannot predict the exact bottom as it is typically a process, and the ultimate bottom may only come when investors have lost all hope of finding it. Unfortunately, with investors still asking "when can I/what should I buy?" it appears that this moment is not yet imminent.

*Defensive positions in a portfolio are investments that aim to protect against market downturns. Examples include bonds, gold, defensive stocks, and cash.

The Content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained on our Site constitutes a solicitation, recommendation, endorsement, or offer by EF or any third party service provider to buy or sell any securities or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction.